Introduction

Uncertainty is a constant companion for organizations, irrespective of their scale or sector. Whether it's a global corporation or a local startup, risks abound in various forms—market fluctuations, regulatory changes, geopolitical upheaval, technological disruptions, or unexpected events like natural disasters. According to a 2025 global risk survey, over 60% of business leaders say emerging risks are increasing faster than their organizations’ ability to identify and respond to them, highlighting a clear gap in early risk detection capabilities.

These risks are genuinely tangible factors that can directly influence business outcomes and strategies, and understanding these elements is a fundamental necessity for survival and success.

This article is designed for Chief Risk Officers, risk leaders, and ERM teams seeking to strengthen their risk identification capabilities. In this piece, we will discuss risk identification and its important, key strategies and best practices for effectively identifying organizational risks, and more.

Key Takeaways

- Risk identification is the foundational step in risk management, crucial for understanding and addressing potential threats that could impact organizational objectives.

- Early risk identification enables proactive decision-making, enhances preparedness through contingency planning, optimizes resource allocation, and provides a competitive advantage by fostering resilience.

- The process of identifying risks involves defining project scope, brainstorming with teams, analyzing historical data, conducting interviews, and leveraging expertise to comprehensively identify potential risks.

- SWOT analysis, FMEA (Failure Mode and Effect Analysis), and scenario analysis are some of the well-known techniques for effective risk identification.

What is Risk Identification?

Risk identification is the systematic process of spotting potential threats that could impact an organization's objectives. Such risks can arise from internal operations, market changes, regulatory shifts, or external factors like natural disasters or regional upheavals.

The goal is to recognize and document possible disruptions before they affect the business.

Risk identification is the process of determining potential risks faced by an organization. It is the foundational step in the journey towards robust risk management. It involves systematically recognizing and cataloging potential threats that could adversely affect an organization's ability to achieve its objectives.

This approach is the cornerstone upon which a strategic and comprehensive risk management program is built. By identifying risks early, organizations can devise strategies to avoid or mitigate their impact, thereby safeguarding their assets, reputation, and future success.

What are the Benefits of Risk Identification?

Risk identification plays a significant role in actively reducing the negative impact of potential threats while also uncovering opportunities to enhance project outcomes. By identifying risks early, businesses can better prepare for challenges and make informed decisions on risk management strategies, ultimately improving the likelihood of success and achieving objectives more efficiently.

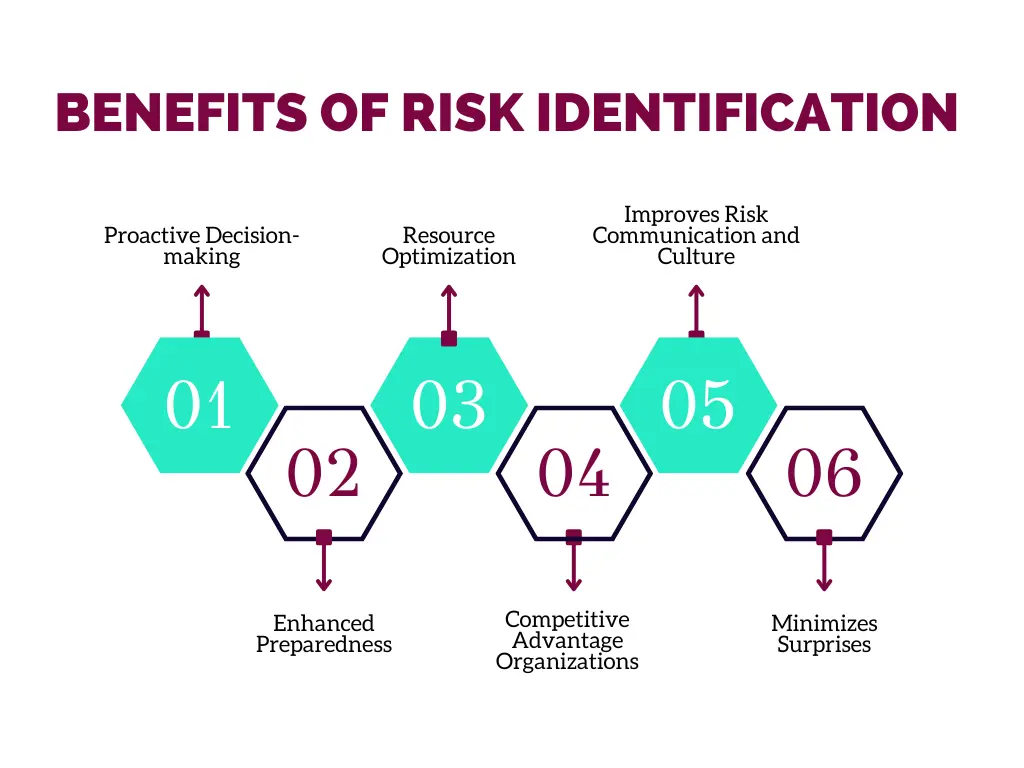

Some of the important benefits of risk identification are as follows:

- Proactive Decision-making Early identification of potential risks empowers organizations to make informed, forward-looking decisions. Instead of being reactive to crises as they unfold, companies can adopt a proactive stance, anticipating challenges and devising strategies to circumvent or tackle them effectively.

- Enhanced Preparedness Knowledge of the potential risks on the horizon enables organizations to strengthen risk preparedness. This may involve setting up contingency plans, allocating resources more wisely, or instituting crisis management protocols, thereby ensuring that the entity is better positioned to withstand adversities.

- Resource Optimization: Identifying risks early helps in prioritizing the allocation of resources—both financial and human—to areas where they are most needed. This ensures that efforts are concentrated on fortifying parts of the organization that are most vulnerable to potential threats.

- Competitive Advantage Organizations that excel in identifying and managing risks can navigate challenges more effectively than their competitors. This agility and resilience can translate into a competitive edge, making them more attractive to investors, partners, and customers.

- Improves Risk Communication and Culture When risk identification is integrated into the organization's processes, it fosters a culture where risks are openly discussed and addressed. This openness only improves teamwork, as employees understand the importance of their roles in managing risks, and it ensures that all levels of the organization are aligned in their approach to risk management.

- Minimizes Surprises By uncovering risks before they manifest into significant issues, organizations can avoid being caught off-guard. This reduces the likelihood of scrambling for solutions under pressure, which often leads to suboptimal outcomes.

Process of Risk Identification

The risk identification process begins by defining the project scope to focus on objectives and assess potential risks. Team brainstorming sessions leverage collective insights to uncover a range of risks. Historical data analysis provides insights from past experiences, aiding in anticipating future risks. Stakeholder interviews and expert consultations reveal hidden and nuanced risk factors.

Here’s an overview of the general steps involved:

- Defining Project Scope Before plunging into risk identification, it's crucial to delineate the boundaries of the project or the operational area being assessed. This involves understanding the project's objectives, deliverables, timelines, and resources. A clear scope helps focus the risk identification process, ensuring that all potential risks are relevant to the context at hand.

- Engaging Key Stakeholders in Brainstorming These sessions leverage the collective experience and insights of the team to surface a broad range of potential risks. It's a creative process that encourages open communication and the consideration of all possible risk sources, whether internal or external, financial, strategic, operational, or compliance-related.

- Consulting Historical Data Historical data and past project reports are goldmines of information for identifying potential risks. They offer insights into what went wrong (or right) in similar scenarios in the past, providing a valuable perspective for anticipating future risks.

- Interviews and Surveys Engaging directly with employees, customers, and other stakeholders through interviews and surveys can unearth risks that might not be immediately obvious. These tools provide nuanced understanding from different perspectives, highlighting risks that could have been overlooked.

- Utilizing Expertise For areas that require specialized knowledge, consulting with experts can shine a light on specific risks. Their expertise can help identify nuances and subtleties in risk factors that non-experts might miss.

Common Mistakes in Risk Identification

Here are some errors organizations might commit while carrying out the process of risk identification:

Underestimating the Impact of "Low-Risk" Events

Often, organizations focus on high-risk scenarios and overlook the seemingly insignificant ones. While a low-probability risk might appear harmless, when combined with others, it can lead to a significant negative impact. Failing to account for these "low-risk" events can leave vulnerabilities in your strategy.

Relying Too Heavily on Historical Data

Using past data to identify risks can surely be helpful, but it can also be a trap. Relying solely on historical trends may cause businesses to miss emerging risks - especially in fast-changing industries where new threats constantly arise. A forward-looking approach is essential for comprehensive risk identification.

Failing to Involve the Right Stakeholders

Risk identification can’t be a top-down process. When key stakeholders such as employees, customers, or external partners are not included, it can result in blind spots. Involving a diverse group ensures that you identify risks from multiple angles, uncovering potential threats that may have otherwise been missed.

Not Updating the Risk Register

Risk identification is an ongoing process. A common mistake is assuming that once risks are identified, they are set in stone. Businesses that fail to regularly update their risk register may overlook emerging risks or fail to adapt to changing circumstances, leaving them unprepared for new challenges.

Overlooking the Human Factor

It's easy to focus on systems, processes, and technology, but the human element is just as important. Mistakes such as employee negligence, human error, or even malicious actions can be a significant source of risk. Overlooking these factors can lead to costly surprises down the line.

What are Some Pros/Cons of Risk Methods?

Different risk identification methods offer different strengths. The right choice depends on organizational maturity, data availability, and the type of risks being examined.

| Risk Identification Method | Pros | Cons |

| Workshops and Brainstorming Sessions | Encourages cross-functional insight and collective ownership. Surfaces risks that may not appear in reports. | Can be subjective. Outcomes depend on participant expertise and facilitation quality. |

| Interviews with Key Stakeholders | Provides deep operational insight. Reveals hidden or emerging risks. | Time-intensive. May reflect individual bias or limited perspective. |

| Historical Loss Analysis | Data-driven and evidence-based. Helps identify recurring patterns. | Focuses on past events. May miss emerging or non-traditional risks. |

| Risk Surveys and Questionnaires | Scalable across large organizations. Creates structured documentation. | Responses may lack depth. Risk of inconsistent interpretation. |

| Scenario Analysis and Stress Testing | Useful for low-frequency, high-impact risks. Encourages forward-looking thinking. | Requires expertise and structured assumptions. May involve estimation uncertainty. |

| Data Analytics and Monitoring Tools | Detects trends and anomalies quickly. Supports continuous identification. | Dependent on data quality and system integration. May require technical investment. |

Key Strategies for Effective Risk Identification

Strategies for risk identification involve systematic approaches aimed at uncovering potential risks, threats, and vulnerabilities within an organization. Here are some effective strategies organizations can use to identify risks:

SWOT Analysis

SWOT, which stands for Strengths, Weaknesses, Opportunities, and Threats, is a tool that helps organizations understand internal and external factors that could impact their objectives.

- Strengths: It involves understanding what an organization excels at or possesses uniquely compared to competitors. While strengths are positive, identifying them helps in recognizing how these advantages can be preserved, utilized more effectively, or even leveraged to mitigate potential risks.

- Weaknesses: The next step focuses on internal vulnerabilities. It's about honesty and openness in recognizing the areas where the organization might be lacking or could improve. Understanding weaknesses is crucial for anticipating risks that could exploit these vulnerabilities.

- Opportunities: This aspect looks outward, identifying potential chances for the organization to grow or improve its position. By recognizing opportunities, organizations can also spot risks involved in pursuing them or the risk of missing out on them due to inaction.

- Threats: Finally, identifying external threats is critical. These could include anything from changes in market conditions, and legal challenges, to technological advancements that could disrupt the business model.

FMEA (Failure Mode and Effect Analysis)

Originating from the aerospace industry in the 1960s and subsequently embraced across various sectors, Failure Mode and Effect Analysis (FMEA) is a systematic, step-by-step approach aimed at identifying all possible failures in a design, a manufacturing or assembly process, or a product or service.

Failure modes imply the ways or modes in which something might fail. Failures are classified according to their severity, occurrence, and detection probabilities, helping prioritize risk reduction efforts on the most significant problems.

Implementing FMEA involves several critical steps:

- First, define the scope of the FMEA project—whether it's for a process, product, or service.

- Next, assemble a cross-functional team—having diverse perspectives is crucial.

- Then, systematically identify all potential failure modes, their effects, and causes, and assess their severity, occurrence, and detection to prioritize actions.

This rigorous method illuminates risks that might not be apparent at a cursory glance and promotes a proactive culture of risk management. It empowers organizations to mitigate risks effectively, potentially saving significant resources and safeguarding their reputation.

Scenario Analysis

Scenario planning and analysis, another robust strategy, moves away from traditional predictive models that rely heavily on past data. It acknowledges the unpredictable nature of the future and instead, creates a variety of plausible scenarios that could impact the organization.

This technique involves identifying external forces and examining how combinations of these forces could change the future. The resulting scenarios help organizations visualize the potential challenges and opportunities they might face.

The process of scenario planning encourages organizations to think the unthinkable, thus expanding their horizon of preparedness. It goes beyond mere risk avoidance, enabling the development of flexible strategies that can be adapted to various future states, thereby saving organizations a lot of time and assets.

How Can Technology Support Risk Identification?

Surface Weak Signals Before They Become Incidents

Modern systems can detect small behavioural drifts across processes. A slight rise in approval overrides or near-miss events may signal cultural or control fatigue. These weak signals often precede major failures.

Map Interdependencies Across The Enterprise

Risk rarely exists in isolation. Graph-based tools can show how a vendor outage connects to liquidity exposure or customer churn. Seeing these hidden linkages reveals systemic risk that siloed reviews miss.

Turn Unstructured Noise Into Structured Insight

Emails, support tickets, audit comments, and regulatory updates contain risk clues. Text analysis tools convert this narrative data into themes and trend indicators. This expands risk visibility beyond formal reporting channels.

Track Decision Patterns, Not Just Outcomes

Technology can analyse decision velocity, approval cycles, and exception frequency. Repeated deviations from policy may reveal emerging governance risk before financial impact appears.

Create A Feedback Loop From Incidents To Prevention

Incident data can be mined to identify recurring root causes across business units. Instead of treating each event as isolated, systems can cluster patterns and highlight structural weaknesses.

What are the Different Types of Risks Companies May Face?

Here are the different types of risks organizations may face:

Strategic Risks:

These risks arise from the decisions your organization makes about its business direction. They can include entering a new market, introducing a new product, or altering business models. Poor strategic choices can lead to significant setbacks, from missed opportunities to financial losses.

Operational Risks:

Operational risks stem from internal processes, people, or systems failing to perform as expected. These can range from supply chain disruptions to inefficient workflows or even technical failures that impact the business. Handling a risk of this nature is all about streamlining your operations and ensuring consistency.

Financial Risks:

Financial risks are tied to uncertainties that could affect an organization’s bottom line, such as fluctuating market conditions, changes in interest rates, or credit risk. These risks can dramatically affect profitability, so it's essential to always stay on top of financial planning and forecasting.

Compliance Risks:

They arise from the possibility of failing to adhere to laws, regulations, and industry standards. For businesses in heavily regulated sectors, these risks can result in hefty fines, reputational damage, and legal troubles.

Reputational Risks:

In an era where information spreads like wildfire, a company's reputation is fragile. Reputational risks arise when customers, employees, or the media react negatively to a scandal, poor customer experience, or mishandled public issue.

Environmental Risks:

They can include the growing impacts of climate change, shifting weather patterns, and even regulatory changes aimed at protecting the environment. For industries such as agriculture, construction, and manufacturing, these risks can severely disrupt supply chains, delay production, or increase costs.

Market Risks:

Market risks are tricky because they’re driven by the unpredictable nature of consumer trends, competitor innovations, and even political or economic upheavals. Risk management here is less about avoiding change and more about adapting to it quickly and effectively.

Conclusion

The journey of risk identification is intricate and multi-dimensional, demanding both detailed scrutiny and broad vision. When working in environments where risks are both omnipresent and ever-evolving, having the right strategies in place is crucial.

More importantly, leveraging the capabilities of an integrated risk management solution like MetricStream's can transform risk management from a daunting task into a strategic advantage. MetricStream’s tools elevate traditional approaches by providing a centralized platform for capturing and analyzing risk data, facilitating cross-functional collaboration, and offering actionable insights through advanced analytics and reporting features.

It doesn't promise a world free of risks—no solution can. What it does offer, however, is a smarter way to identify, assess, and manage those risks, giving your business the best chance at success.

Uncertainty is a constant companion for organizations, irrespective of their scale or sector. Whether it's a global corporation or a local startup, risks abound in various forms—market fluctuations, regulatory changes, geopolitical upheaval, technological disruptions, or unexpected events like natural disasters. According to a 2025 global risk survey, over 60% of business leaders say emerging risks are increasing faster than their organizations’ ability to identify and respond to them, highlighting a clear gap in early risk detection capabilities.

These risks are genuinely tangible factors that can directly influence business outcomes and strategies, and understanding these elements is a fundamental necessity for survival and success.

This article is designed for Chief Risk Officers, risk leaders, and ERM teams seeking to strengthen their risk identification capabilities. In this piece, we will discuss risk identification and its important, key strategies and best practices for effectively identifying organizational risks, and more.

- Risk identification is the foundational step in risk management, crucial for understanding and addressing potential threats that could impact organizational objectives.

- Early risk identification enables proactive decision-making, enhances preparedness through contingency planning, optimizes resource allocation, and provides a competitive advantage by fostering resilience.

- The process of identifying risks involves defining project scope, brainstorming with teams, analyzing historical data, conducting interviews, and leveraging expertise to comprehensively identify potential risks.

- SWOT analysis, FMEA (Failure Mode and Effect Analysis), and scenario analysis are some of the well-known techniques for effective risk identification.

Risk identification is the systematic process of spotting potential threats that could impact an organization's objectives. Such risks can arise from internal operations, market changes, regulatory shifts, or external factors like natural disasters or regional upheavals.

The goal is to recognize and document possible disruptions before they affect the business.

Risk identification is the process of determining potential risks faced by an organization. It is the foundational step in the journey towards robust risk management. It involves systematically recognizing and cataloging potential threats that could adversely affect an organization's ability to achieve its objectives.

This approach is the cornerstone upon which a strategic and comprehensive risk management program is built. By identifying risks early, organizations can devise strategies to avoid or mitigate their impact, thereby safeguarding their assets, reputation, and future success.

Risk identification plays a significant role in actively reducing the negative impact of potential threats while also uncovering opportunities to enhance project outcomes. By identifying risks early, businesses can better prepare for challenges and make informed decisions on risk management strategies, ultimately improving the likelihood of success and achieving objectives more efficiently.

Some of the important benefits of risk identification are as follows:

- Proactive Decision-making Early identification of potential risks empowers organizations to make informed, forward-looking decisions. Instead of being reactive to crises as they unfold, companies can adopt a proactive stance, anticipating challenges and devising strategies to circumvent or tackle them effectively.

- Enhanced Preparedness Knowledge of the potential risks on the horizon enables organizations to strengthen risk preparedness. This may involve setting up contingency plans, allocating resources more wisely, or instituting crisis management protocols, thereby ensuring that the entity is better positioned to withstand adversities.

- Resource Optimization: Identifying risks early helps in prioritizing the allocation of resources—both financial and human—to areas where they are most needed. This ensures that efforts are concentrated on fortifying parts of the organization that are most vulnerable to potential threats.

- Competitive Advantage Organizations that excel in identifying and managing risks can navigate challenges more effectively than their competitors. This agility and resilience can translate into a competitive edge, making them more attractive to investors, partners, and customers.

- Improves Risk Communication and Culture When risk identification is integrated into the organization's processes, it fosters a culture where risks are openly discussed and addressed. This openness only improves teamwork, as employees understand the importance of their roles in managing risks, and it ensures that all levels of the organization are aligned in their approach to risk management.

- Minimizes Surprises By uncovering risks before they manifest into significant issues, organizations can avoid being caught off-guard. This reduces the likelihood of scrambling for solutions under pressure, which often leads to suboptimal outcomes.

The risk identification process begins by defining the project scope to focus on objectives and assess potential risks. Team brainstorming sessions leverage collective insights to uncover a range of risks. Historical data analysis provides insights from past experiences, aiding in anticipating future risks. Stakeholder interviews and expert consultations reveal hidden and nuanced risk factors.

Here’s an overview of the general steps involved:

- Defining Project Scope Before plunging into risk identification, it's crucial to delineate the boundaries of the project or the operational area being assessed. This involves understanding the project's objectives, deliverables, timelines, and resources. A clear scope helps focus the risk identification process, ensuring that all potential risks are relevant to the context at hand.

- Engaging Key Stakeholders in Brainstorming These sessions leverage the collective experience and insights of the team to surface a broad range of potential risks. It's a creative process that encourages open communication and the consideration of all possible risk sources, whether internal or external, financial, strategic, operational, or compliance-related.

- Consulting Historical Data Historical data and past project reports are goldmines of information for identifying potential risks. They offer insights into what went wrong (or right) in similar scenarios in the past, providing a valuable perspective for anticipating future risks.

- Interviews and Surveys Engaging directly with employees, customers, and other stakeholders through interviews and surveys can unearth risks that might not be immediately obvious. These tools provide nuanced understanding from different perspectives, highlighting risks that could have been overlooked.

- Utilizing Expertise For areas that require specialized knowledge, consulting with experts can shine a light on specific risks. Their expertise can help identify nuances and subtleties in risk factors that non-experts might miss.

Here are some errors organizations might commit while carrying out the process of risk identification:

Underestimating the Impact of "Low-Risk" Events

Often, organizations focus on high-risk scenarios and overlook the seemingly insignificant ones. While a low-probability risk might appear harmless, when combined with others, it can lead to a significant negative impact. Failing to account for these "low-risk" events can leave vulnerabilities in your strategy.

Relying Too Heavily on Historical Data

Using past data to identify risks can surely be helpful, but it can also be a trap. Relying solely on historical trends may cause businesses to miss emerging risks - especially in fast-changing industries where new threats constantly arise. A forward-looking approach is essential for comprehensive risk identification.

Failing to Involve the Right Stakeholders

Risk identification can’t be a top-down process. When key stakeholders such as employees, customers, or external partners are not included, it can result in blind spots. Involving a diverse group ensures that you identify risks from multiple angles, uncovering potential threats that may have otherwise been missed.

Not Updating the Risk Register

Risk identification is an ongoing process. A common mistake is assuming that once risks are identified, they are set in stone. Businesses that fail to regularly update their risk register may overlook emerging risks or fail to adapt to changing circumstances, leaving them unprepared for new challenges.

Overlooking the Human Factor

It's easy to focus on systems, processes, and technology, but the human element is just as important. Mistakes such as employee negligence, human error, or even malicious actions can be a significant source of risk. Overlooking these factors can lead to costly surprises down the line.

Different risk identification methods offer different strengths. The right choice depends on organizational maturity, data availability, and the type of risks being examined.

| Risk Identification Method | Pros | Cons |

| Workshops and Brainstorming Sessions | Encourages cross-functional insight and collective ownership. Surfaces risks that may not appear in reports. | Can be subjective. Outcomes depend on participant expertise and facilitation quality. |

| Interviews with Key Stakeholders | Provides deep operational insight. Reveals hidden or emerging risks. | Time-intensive. May reflect individual bias or limited perspective. |

| Historical Loss Analysis | Data-driven and evidence-based. Helps identify recurring patterns. | Focuses on past events. May miss emerging or non-traditional risks. |

| Risk Surveys and Questionnaires | Scalable across large organizations. Creates structured documentation. | Responses may lack depth. Risk of inconsistent interpretation. |

| Scenario Analysis and Stress Testing | Useful for low-frequency, high-impact risks. Encourages forward-looking thinking. | Requires expertise and structured assumptions. May involve estimation uncertainty. |

| Data Analytics and Monitoring Tools | Detects trends and anomalies quickly. Supports continuous identification. | Dependent on data quality and system integration. May require technical investment. |

Strategies for risk identification involve systematic approaches aimed at uncovering potential risks, threats, and vulnerabilities within an organization. Here are some effective strategies organizations can use to identify risks:

SWOT Analysis

SWOT, which stands for Strengths, Weaknesses, Opportunities, and Threats, is a tool that helps organizations understand internal and external factors that could impact their objectives.

- Strengths: It involves understanding what an organization excels at or possesses uniquely compared to competitors. While strengths are positive, identifying them helps in recognizing how these advantages can be preserved, utilized more effectively, or even leveraged to mitigate potential risks.

- Weaknesses: The next step focuses on internal vulnerabilities. It's about honesty and openness in recognizing the areas where the organization might be lacking or could improve. Understanding weaknesses is crucial for anticipating risks that could exploit these vulnerabilities.

- Opportunities: This aspect looks outward, identifying potential chances for the organization to grow or improve its position. By recognizing opportunities, organizations can also spot risks involved in pursuing them or the risk of missing out on them due to inaction.

- Threats: Finally, identifying external threats is critical. These could include anything from changes in market conditions, and legal challenges, to technological advancements that could disrupt the business model.

FMEA (Failure Mode and Effect Analysis)

Originating from the aerospace industry in the 1960s and subsequently embraced across various sectors, Failure Mode and Effect Analysis (FMEA) is a systematic, step-by-step approach aimed at identifying all possible failures in a design, a manufacturing or assembly process, or a product or service.

Failure modes imply the ways or modes in which something might fail. Failures are classified according to their severity, occurrence, and detection probabilities, helping prioritize risk reduction efforts on the most significant problems.

Implementing FMEA involves several critical steps:

- First, define the scope of the FMEA project—whether it's for a process, product, or service.

- Next, assemble a cross-functional team—having diverse perspectives is crucial.

- Then, systematically identify all potential failure modes, their effects, and causes, and assess their severity, occurrence, and detection to prioritize actions.

This rigorous method illuminates risks that might not be apparent at a cursory glance and promotes a proactive culture of risk management. It empowers organizations to mitigate risks effectively, potentially saving significant resources and safeguarding their reputation.

Scenario Analysis

Scenario planning and analysis, another robust strategy, moves away from traditional predictive models that rely heavily on past data. It acknowledges the unpredictable nature of the future and instead, creates a variety of plausible scenarios that could impact the organization.

This technique involves identifying external forces and examining how combinations of these forces could change the future. The resulting scenarios help organizations visualize the potential challenges and opportunities they might face.

The process of scenario planning encourages organizations to think the unthinkable, thus expanding their horizon of preparedness. It goes beyond mere risk avoidance, enabling the development of flexible strategies that can be adapted to various future states, thereby saving organizations a lot of time and assets.

Surface Weak Signals Before They Become Incidents

Modern systems can detect small behavioural drifts across processes. A slight rise in approval overrides or near-miss events may signal cultural or control fatigue. These weak signals often precede major failures.

Map Interdependencies Across The Enterprise

Risk rarely exists in isolation. Graph-based tools can show how a vendor outage connects to liquidity exposure or customer churn. Seeing these hidden linkages reveals systemic risk that siloed reviews miss.

Turn Unstructured Noise Into Structured Insight

Emails, support tickets, audit comments, and regulatory updates contain risk clues. Text analysis tools convert this narrative data into themes and trend indicators. This expands risk visibility beyond formal reporting channels.

Track Decision Patterns, Not Just Outcomes

Technology can analyse decision velocity, approval cycles, and exception frequency. Repeated deviations from policy may reveal emerging governance risk before financial impact appears.

Create A Feedback Loop From Incidents To Prevention

Incident data can be mined to identify recurring root causes across business units. Instead of treating each event as isolated, systems can cluster patterns and highlight structural weaknesses.

Here are the different types of risks organizations may face:

Strategic Risks:

These risks arise from the decisions your organization makes about its business direction. They can include entering a new market, introducing a new product, or altering business models. Poor strategic choices can lead to significant setbacks, from missed opportunities to financial losses.

Operational Risks:

Operational risks stem from internal processes, people, or systems failing to perform as expected. These can range from supply chain disruptions to inefficient workflows or even technical failures that impact the business. Handling a risk of this nature is all about streamlining your operations and ensuring consistency.

Financial Risks:

Financial risks are tied to uncertainties that could affect an organization’s bottom line, such as fluctuating market conditions, changes in interest rates, or credit risk. These risks can dramatically affect profitability, so it's essential to always stay on top of financial planning and forecasting.

Compliance Risks:

They arise from the possibility of failing to adhere to laws, regulations, and industry standards. For businesses in heavily regulated sectors, these risks can result in hefty fines, reputational damage, and legal troubles.

Reputational Risks:

In an era where information spreads like wildfire, a company's reputation is fragile. Reputational risks arise when customers, employees, or the media react negatively to a scandal, poor customer experience, or mishandled public issue.

Environmental Risks:

They can include the growing impacts of climate change, shifting weather patterns, and even regulatory changes aimed at protecting the environment. For industries such as agriculture, construction, and manufacturing, these risks can severely disrupt supply chains, delay production, or increase costs.

Market Risks:

Market risks are tricky because they’re driven by the unpredictable nature of consumer trends, competitor innovations, and even political or economic upheavals. Risk management here is less about avoiding change and more about adapting to it quickly and effectively.

The journey of risk identification is intricate and multi-dimensional, demanding both detailed scrutiny and broad vision. When working in environments where risks are both omnipresent and ever-evolving, having the right strategies in place is crucial.

More importantly, leveraging the capabilities of an integrated risk management solution like MetricStream's can transform risk management from a daunting task into a strategic advantage. MetricStream’s tools elevate traditional approaches by providing a centralized platform for capturing and analyzing risk data, facilitating cross-functional collaboration, and offering actionable insights through advanced analytics and reporting features.

It doesn't promise a world free of risks—no solution can. What it does offer, however, is a smarter way to identify, assess, and manage those risks, giving your business the best chance at success.

Frequently Asked Questions

Components of risk identification include:

Risk statement

Basic identification

Detailed identification

External cross-check

Internal cross-check

Statement finalization.

Ways to identify risk include:

Brainstorming.

Documentation review.

Analyzing project documents and historical data.

Expert interviews.

Checklists and templates.

The following are the stages of risk identification:

Planning

Identification

Assessment and analysis

Review and validation

Communication across teams.

Establish Context: Define the scope and environment.

Identify Risks: Spot potential threats and opportunities.

Analyze Risks: Assess likelihood and impact.

Evaluate Interactions: Understand how risks relate to each other.

Document: Record identified risks for future reference.

Risk identification is the structured process of recognizing events or conditions that could affect strategic objectives. It focuses on spotting uncertainties before they materialize into losses. In ERM, it forms the foundation for analysis, prioritisation, and mitigation.

Common techniques include workshops, interviews, process mapping, scenario analysis, and review of incident data. More advanced approaches use analytics, trend monitoring, and external intelligence feeds. The most effective programs combine qualitative insight with data-driven signals.

Risk identification answers the question, “What could go wrong?” Risk assessment evaluates how likely and impactful those risks are. Identification is discovery. Assessment is measurement.

Many organizations rely only on past incidents and overlook emerging threats. Others treat it as a one-time exercise rather than an ongoing process. Narrow participation and lack of cross-functional input also weaken results.

Start by defining categories aligned with business objectives. Document each identified risk with a clear description, source, and potential impact. Assign ownership and link it to related processes or controls for traceability.

At least annually and whenever there is significant business change. Mergers, new technology adoption, regulatory shifts, or market disruption should trigger a fresh review. Continuous monitoring can supplement formal cycles.

Stakeholders provide operational insight and contextual awareness. Front-line teams often see early warning signs before leadership does. Broad participation improves completeness and reduces blind spots.

Project risks can impact stakeholders through financial loss, delays, compliance issues, quality failures, or reputational damage. Different stakeholders face different exposures, so identifying these impacts early helps protect expectations, trust, and investment value.

Risk assessments should be reviewed regularly and updated whenever there are significant changes in scope, resources, timelines, or external conditions. Fast-moving projects may require more frequent reviews to stay aligned with emerging risks.

Common risks in new projects include unclear scope, budget overruns, resource gaps, unrealistic timelines, vendor issues, and regulatory or technical uncertainties. Early risk identification helps address these vulnerabilities before they escalate.